Introduction

Building a secure retirement is one of the most important financial goals of your life. However, many people stumble due to common retirement planning mistakes that can quietly derail even the best intentions. By learning about retirement planning mistakes early, you can recognize and avoid errors before they become serious problems. Using insights from retirement planning mistakes allows you to make informed decisions and stay on track toward your goals. Understanding retirement planning mistakes ensures your journey to financial independence is smoother and more successful, giving you confidence in every step.

What Are Retirement Planning Mistakes?

Retirement planning mistakes are common errors in strategy or behavior that can significantly impact your financial future. By understanding retirement planning mistakes, you can identify habits and decisions that silently erode your nest egg. Using insights from retirement planning mistakes helps you avoid procrastination, high fees, and other pitfalls that can derail your retirement goals. Learning from retirement planning mistakes ensures you make smarter choices today, turning the dream of a comfortable future into a secure reality.

Understanding retirement planning mistakes is critical because the stakes for your future are high. Many people fall behind on their retirement savings due to common retirement planning mistakes they don’t even realize they’re making. By learning to spot retirement planning mistakes early, you can avoid traps that silently undermine your financial goals. Using insights from retirement planning mistakes allows you to build a stronger, more resilient plan and take control of your retirement with confidence.

Why Avoiding These Mistakes is Crucial for Your Future

Your future financial freedom depends on avoiding these common pitfalls. The consequences of these errors can be devastating.

Protect Your Nest Egg from Silent Killers

Mistakes like paying high fees or underestimating inflation don’t feel painful in the short term, but over decades, they can silently erase hundreds of thousands of dollars from your portfolio. Avoiding them is like plugging a slow, steady leak in your financial boat.

Maximize the Power of Compound Growth

The biggest mistakes—starting late and not saving enough—are direct attacks on the power of compound interest. Every dollar you fail to save in your 20s is a dollar that doesn’t have 40 years to grow. Avoiding these errors ensures you give your money the maximum possible time to work for you.

Reduce Stress and Build Financial Confidence

Navigating your financial life with a clear understanding of what *not* to do is incredibly empowering. It reduces the anxiety that comes with uncertainty and gives you the confidence to make smart, proactive decisions about your money. For more on building a secure future, check out this valuable resource.

The Top 7 Retirement Planning Mistakes to Avoid

Here are the seven most common and damaging mistakes that can derail your journey to a secure retirement.

Mistake #1: Starting Too Late

This is, without a doubt, the single biggest mistake. The math is unforgiving. Thanks to compound interest, the money you save in your 20s is exponentially more powerful than the money you save in your 40s. Delaying by even a few years can be the difference between a comfortable retirement and having to work well into your 70s.

Mistake #2: Ignoring the 401(k) Match

If your employer offers a 401(k) match, it is the best investment you will ever make. It’s a 100% return on your money, guaranteed. Failing to contribute at least enough to get the full match is like lighting a pile of free money on fire. This should be your absolute first financial priority.

Mistake #3: Paying High Investment Fees

Fees may seem small—1% sounds harmless—but over 30 or 40 years, they can consume a massive portion of your nest egg. A 1% fee can reduce your final portfolio value by nearly a third. Always opt for low-cost index funds or ETFs with expense ratios below 0.5% whenever possible.

Mistake #4: Trying to Time the Market

It’s tempting to try to sell when the market is high and buy when it’s low. But even professional investors consistently fail at this. The most effective strategy is to invest a consistent amount of money every single month, regardless of what the market is doing. This is called dollar-cost averaging, and it’s your best defense against market volatility.

Mistake #5: Being Too Conservative (or Too Aggressive)

Your investment strategy should match your age. If you’re in your 20s, your portfolio should be almost entirely in stocks for long-term growth. If you’re in your 60s, it should be more balanced with bonds to preserve your capital. Being too conservative when you’re young means you’ll miss out on growth, while being too aggressive when you’re older exposes you to unnecessary risk.

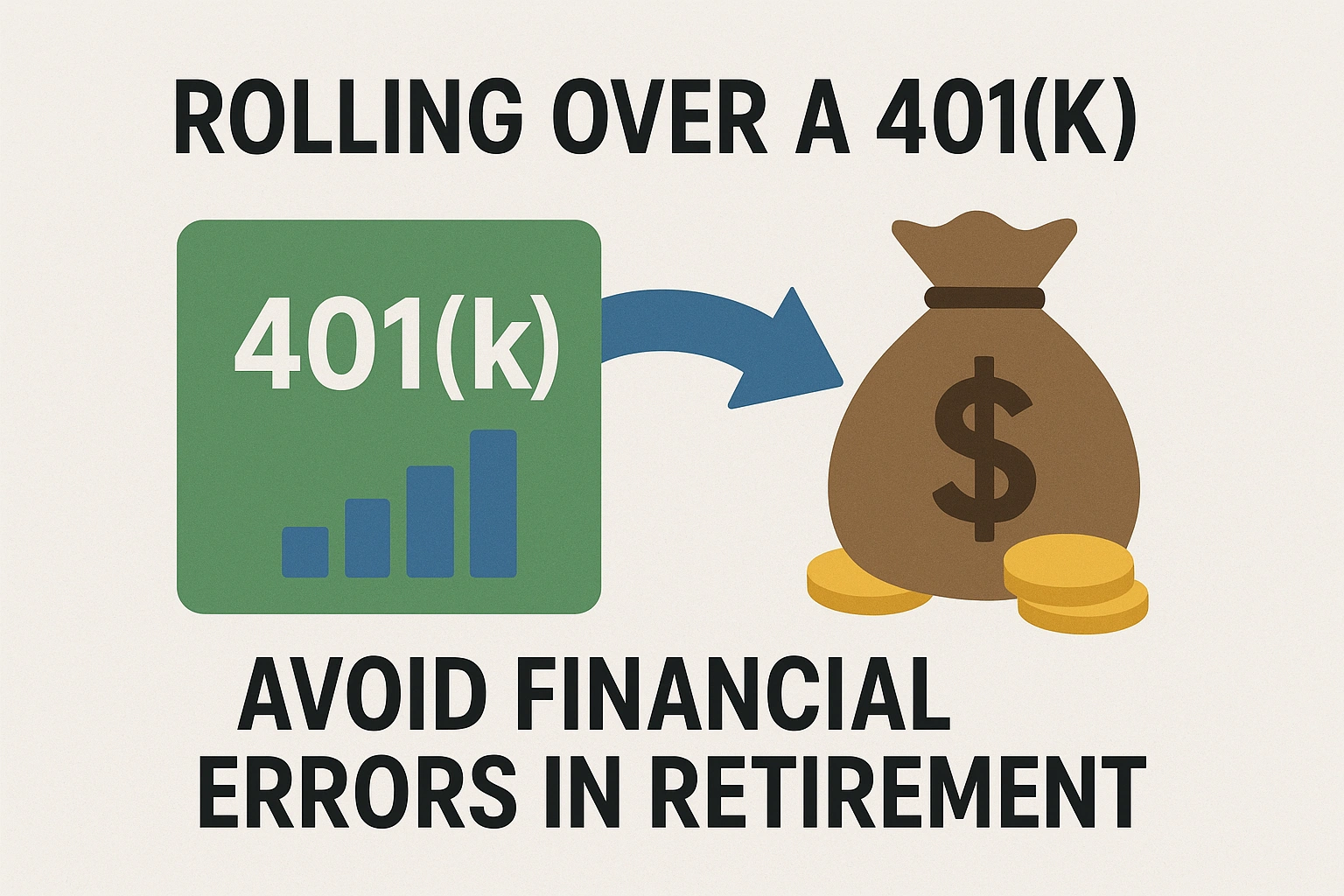

Mistake #6: Cashing Out Your 401(k) When You Change Jobs

This is a catastrophic error. When you leave a job, you will be given the option to cash out your 401(k). If you do, you’ll pay a 10% penalty plus your ordinary income tax rate, and you’ll completely reset the compound growth on that money. Always choose to roll it over into an IRA or your new employer’s 401(k).

Mistake #7: Not Having a Plan

Failing to plan is planning to fail. Without a clear goal and a written strategy, you’re just saving aimlessly. You need to know how much you need to save, how you’re going to save it, and how you’re going to invest it. This is the foundation of all successful **financial planning for retirement**.

How to Correct Your Course

Recognizing a mistake is the first step. Here’s a simple guide to correcting these common errors.

| Mistake | The Simple Fix |

|---|---|

| Starting Too Late | Start today. Open an IRA and set up a small, automatic contribution. The amount is less important than building the habit. |

| Ignoring the Match | Log into your company’s 401(k) portal right now and increase your contribution to get the full match. |

| Paying High Fees | Review your 401(k) investment options and choose the Target-Date Fund or Index Fund with the lowest expense ratio. |

| Trying to Time the Market | Automate your investments so they happen every payday, regardless of the headlines. Stay the course. |

Expert Tips for Success

Avoid these **financial errors in retirement** planning with these pro tips.

- Automate, Automate, Automate: The single best way to avoid behavioral mistakes is to put your savings and investments on autopilot.

- Increase Your Savings Annually: Commit to increasing your savings rate by 1% every year. You’ll barely notice the difference in your paycheck, but it will have a huge impact on your future.

- Keep It Simple: You don’t need a complex portfolio of exotic investments. A simple, diversified portfolio of low-cost index funds is all most people need to succeed.

- Have a “Why”: Get clear on what your dream retirement looks like. Having a compelling vision will keep you motivated to stay disciplined.

“Successful investing is not about genius. It’s about having a sound plan and the discipline to stick with it. The biggest mistakes are almost always emotional, not intellectual.”

– John C. Bogle, Founder of Vanguard

Frequently Asked Questions (FAQ)

Q: What is the single biggest retirement planning mistake?

A: The single biggest and most common mistake is simply starting too late. Because of the power of compound interest, every year of delay in your 20s and 30s can cost you tens or even hundreds of thousands of dollars in future growth. It’s a mathematical hole that becomes very difficult to dig out of.

Q: Is cashing out a 401(k) when I change jobs a big deal?

A: Yes, it is a catastrophic mistake. You will pay a 10% penalty plus your ordinary income tax rate on the entire amount, meaning you could lose 30-40% of your savings immediately. It also completely resets the compound growth on that money. You should always roll over an old 401(k) into an IRA or your new employer’s plan.

Q: How do I know if my investment fees are too high?

A: A good rule of thumb is to look for funds with an expense ratio below 0.5%. Low-cost index funds are often below 0.1%. If the funds in your 401(k) have expense ratios of 1% or higher, they are likely too expensive and will significantly erode your returns over time. Use a free tool like Empower’s dashboard to analyze your fees.

Q: What are the most common financial errors in retirement planning?

A: The most common financial errors include starting late, not saving enough to get the full employer 401(k) match, paying high investment fees, being too conservative with investments at a young age, and trying to time the market instead of investing consistently.

Q: Can I fix my retirement plan if I’ve already made some of these mistakes?

A: Absolutely. The best time to correct your course is right now. You can increase your savings rate, switch to lower-cost investments, and create a disciplined plan moving forward. While you can’t get back lost time, you can make powerful changes today that will dramatically improve your future.

Conclusion

The path to a secure retirement is a marathon, not a sprint. By learning about common retirement planning mistakes, you can avoid pitfalls that derail many people. Understanding retirement planning mistakes helps you make disciplined and consistent choices for your future. Using insights from retirement planning mistakes allows you to stay proactive and build a foundation of financial security. Avoiding retirement planning mistakes ensures that each decision you make brings you closer to a retirement of freedom and confidence.